-

Share via:

(651) 552-3681

Home Purchase - Home Refinance

Lending in AZ, CO, FL, IA, MN, ND, SD, Wi

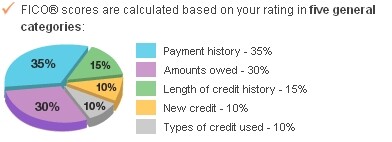

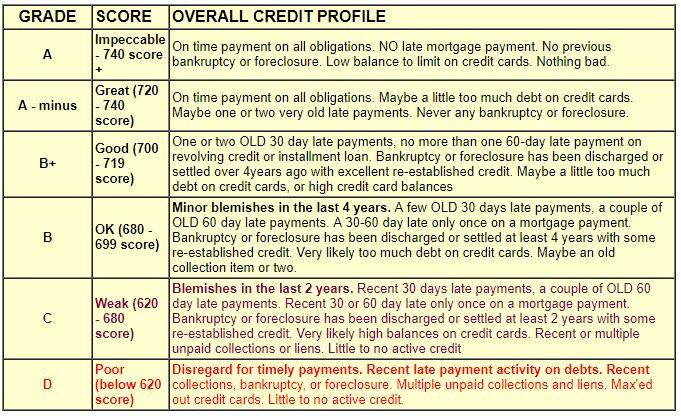

CREDIT SCORE GRADES, and Basic Credit Profiles

Your Credit Report and FICO Credit Score

Its More Important Than You May Think.

Perhaps the most important factor in qualifying for a home loan is your credit score.

Companies such as Experian, TransUnion and Equifax routinely collect and maintain information from credit card companies, banks, department stores, etc., about your payment history, and use it to compile your credit report. In addition, they also collect information from collection agencies, county, state and federal governments, to report items such as collection accounts, judgments and bankruptcies.

The fact is today that many people have blemishes on their credit reports. Whether from divorce, being laid off, or just getting in over their heads, people can begin to re-establish their credit, and eventually qualify to buy a home. Some lending guidelines even allow you to obtain a home loan while currently in a bankruptcy and even stop a foreclosure. Just because your have a few late payments doesn't mean you can't buy a house.

Times have changed. We NO LONGER very many programs for people with bad credit. BUT, don't automatically think you can't get approved... Spend 15 minutes with a Cambria Mortgage professional to make sure. You just might be surprised at what you hear!

Inquiries on your credit report?

Thay are NOT what you think, and 99% of people 99% of the time should never worry about them,

Read our special page dealing with just inquiries on your credit report for more information.

Credit Risk Score?

Some credit grantors make hundreds even thousands of credit granting decisions every day.

To help them make those decisions faster and more objectively, they rely on a computerized process that results in a risk score (or credit score).

Your credit score is often a major factor in qualifying for credit. Lenders can obtain a computerized credit score when they pull your credit. This score is a number which represents an applicant's potential credit worthiness. Although credit scoring has existed for many years, it is gaining popularity in mortgage lending. Many loans are granted or denied on the basis of your credit risk score.

Until recently, Fair Isaac & Company, the creators of the credit scoring model refused to reveal the mysteries of what effects your score (good or bad), and how they arrived at it. Not anymore, click here for details: Credit Score Secrets Revealed. They have also recently began releasing to consumers their scores and interpretive data for a nominal fee.

Many times, information is reported incorrectly on your credit reports. A copy of your credit report can be obtained by clicking the link above. There is a dispute process that allows you to question the accuracy of items on your report, if you feel any items are improperly reported. You don't need to pay a credit repair company. One word of advice. Contact ALL THREE credit reporting agencies. Getting something corrected from one agency doesn't mean it got corrected with the other two!

Get the booklet on Understanding your FICO® score

This booklet provides a thorough description of credit scoring, including ways credit scoring can help you, the relationship between your credit report and your credit score, what a FICO® score considers, and interpreting your score.

Prevent Identify Theft: Opt-out of pre-screened offers.

Stop the flow of junk to your mailbox. The consumer credit reporting industry has provided a way to opt out and remove your name from these lists. You can contact them by phone at 1-888-567-8688 or online at https://www.optoutprescreen.com. It is quick, easy, and free - and valid for 5 years!

Visit Our Social Media Pages

Equal Housing Lender. The Joe Metzler Team at Cambria Mortgage lends in Arizona, Colorado, Florida, Iowa, Minnesota, North Dakota, South Dakota , and Wisconsin only. This is not an offer to lend or to extend credit, nor is this a guaranty of loan approval or commitment to lend. Information here can become out of date, and may no longer be accurate. Products and interest rates are subject to change at any time due to changing market conditions. Not all programs available in all states. Actual rates available to you may vary based upon a number of factors. Consumers must independently verify the accuracy and currency of available mortgage programs. All loan approvals are subject to the borrower(s) satisfying all underwriting guidelines and loan approval conditions and providing an acceptable property, appraisal and title report. Joe Metzler, NMLS 274132, Cambria Mortgage NMLS 322798. © 1998 - 2026.