-

Share via:

(651) 552-3681

Home Purchase - Home Refinance

Lending in AZ, CO, FL, IA, MN, ND, SD, Wi

- Home

- Reviews

- Apply

- Quick Qualify

- Rates & Costs

- Loan Programs

- Bad Credit Loans

- Buying a House

- Commercial / Apartment

- Doctor Loans

- FHA Loans

- Down Payment Assistance

- First Time Home Buyer

- HomeReady

- Investor DSCR Loans

- Luxury home financing

- Jumbo Loans

- Loans for Self Employed

- New Construction Loans

- No Down Payment Loans

- No Doc / Non-QM

- Refinancing

- Contract for Deed Refi

- Renovation Loans

- USDA Loans

- VA Loans

- Client Resources

- After BK or Foreclosure

- The Home Loan Process

- Daily Mortgage News

- Your credit score

- Student loans

- Homebuyer Classes

- Mortgage FAQ

- Glossary of Mortgage Terms

- Use a Bank or Broker?

- Fixed or ARM

- Home Buyers Guide

- Mortgage Rate Locks

- Long Term Rate Locks

- Mortgage Loan Limits

- No Closing Cost Loans

- Get a Second Opinion

- Tips for a smooth closing

- Top Mortgage Mistakes

- Foreclosures / Short Sales

- How to buy foreclosures

- Well and Septic

- Beware Predatory Lenders

- About

- Blog

- My Acct

Navigation- Home

- Reviews

- Apply

- Quick Qualify

- Rates & Costs

- Loan Programs

- Bad Credit Loans

- Buying a House

- Commercial / Apartment

- Doctor Loans

- FHA Loans

- Down Payment Assistance

- First Time Home Buyer

- HomeReady

- Investor DSCR Loans

- Luxury home financing

- Jumbo Loans

- Loans for Self Employed

- New Construction Loans

- No Down Payment Loans

- No Doc / Non-QM

- Refinancing

- Contract for Deed Refi

- Renovation Loans

- USDA Loans

- VA Loans

- Client Resources

- After BK or Foreclosure

- The Home Loan Process

- Daily Mortgage News

- Your credit score

- Student loans

- Homebuyer Classes

- Mortgage FAQ

- Glossary of Mortgage Terms

- Use a Bank or Broker?

- Fixed or ARM

- Home Buyers Guide

- Mortgage Rate Locks

- Long Term Rate Locks

- Mortgage Loan Limits

- No Closing Cost Loans

- Get a Second Opinion

- Tips for a smooth closing

- Top Mortgage Mistakes

- Foreclosures / Short Sales

- How to buy foreclosures

- Well and Septic

- Beware Predatory Lenders

- About

- Blog

- My Acct

How much are closing costs, who pays them, descriptions, breakdowns, and more

A lot of people are involved in the process of buying a house. They include the lender, appraiser, insurance company, your local government, Realtors, inspectors, and an attorney or title company. These people all get paid for their services in the processing, funding, and closing of your mortgage loan.

Part of your Loan Officers responsibility is to explain to you what the services and costs are, and to give you an estimate of the total costs when you apply for a loan. Initially, this will come in the form of an Initial Fees Worksheet. This is only the initial estimate based on your initial inquiry to give you an idea of your total costs. This is not your official Loan Estimate (formerly known as a Good Faith Estimate).

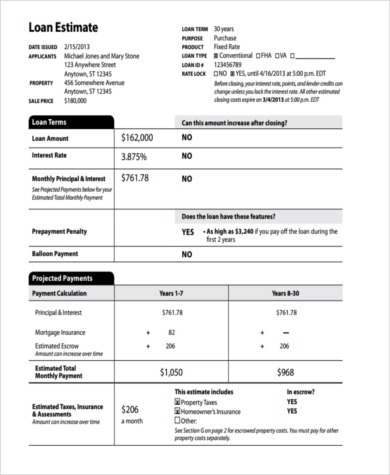

Once you decide to move forward with the lender, as part of their overall application disclosures, you will be given a document titled a Loan Estimate of Closing Costs. This is based on the exact final transaction (exact house, purchase price, locked interest rate, property taxes, etc.). This document is required to be extremely close to your final costs you can expect at closing. Lenders are not allowed to pad, or add onto the costs charged by other parties (like the appraiser), but rather simply pass on what those companies charge. The vast majority of closing costs go to third parties, not your actual lender.

An exact breakdown and description of closing cost charges are at the end of this web page. Lenders and brokers are required by Federal law, known as the Real Estate Settlement Procedures Act (RESPA) to give you a booklet called "Shopping for your home loan - HUD's Settlement Costs Booklet" when applying for a mortgage loan. If they didn't give you one, what are they trying to hide?

Understanding Closing Costs and Fees

Closing costs could be broken down into four categories:

- Discount Points and Origination fees -- Convert these fees into dollar figures to better understand associated costs. For example: One point is 1% of the value of the loan. A discount point or origination fee of one point would equate to $1000 on a $100,000 loan.

- Appraisal, credit report and county/state fees -- These fees do not vary greatly between lenders, but they do vary. Also, you should never ever pay an application fee! The most you should pay a lender 'up-front' is a credit report fee, and that should never exceed $55.00. Paying up-front for your APPRAISAL is also OK.

- Miscellaneous lender charges (application fee, broker fee, funding fee, wire transfer fee, etc.) -- These are the categories where most lenders hide their fees.

- Title/settlement charges-- Include title search, closing fee, survey, title insurance, etc. These fees are paid to a separate company from the lender, so in theory they should be excluded from a lender-to-lender comparison. You should keep in mind that these charges will need to be paid in connection with the loan.

Closing Costs You Can Expect

You can expect most, if not all of these costs when getting a home mortgage loan, and they add up!

Appraisal, Credit Report, Loan Origination, Underwriting, Processing, Title Company Closing Fee, Survey, Lenders Title Insurance, Owners Title Insurance, State Deed taxes, County Recording Fees, transfer taxes, and more.

Then you also have pre-paid items. These are not technically closing costs, but are cost you need to pay one time at or before your closing:

First years home owners insurance, pro-rated property taxes, and days of interest.

Optional Closing Cost:

Discount points, oer simply points. Paid up-front at closing to lower the loans interest rate, either permanently or short-term (like a 2-1 buydown).

How to Compare Closing Costs

Shopping can be confusing. No matter what we're looking for -- from cars to refrigerators -- there's a built-in element of confusion. Why? Lack of knowledge. An unfortunate rule of thumb is that the less we know about something we need to buy, the more we can expect to pay for it.

Shopping for a mortgage is complex at best -- even for the savvy previous home owner. Daily rate changes, time-sensitive lock-in periods, points, lender's fees... plus the emotional element of probably the largest purchase any of us will ever make. Throw in to this already murky stew the ingredients of tricky rate advertising, commissions and costs for everyone and every company who is involved in your transaction, and the obscure differences between rates and fees. It's no mystery that many people settle for a mortgage that exceeds their monetary means out of sheer exasperation!

So, what can we do? The answer is education. If we know how to shop for a mortgage -- the questions to ask, the language to speak, the tools to employ -- we then possess the knowledge to secure the best deal. The following is a simple primer to shine a light of clarity into the darker corners of mortgage lending. Read everything, familiarize yourself with the terminology -- and see how easy it is to secure a competitive mortgage with competitive closing costs.

The Best Interest Rates or the Lowest Closing Costs?

A common mistake shoppers make is to ask: "What's your best interest rate?." It is a logical question to ask, but it does not give the correct response most borrowers need to make a proper decision. Borrowers must understand both rates and fees. Rates are only half the answer to getting the best deal. It is possible end up with the lowest rate but not necessarily the best deal.

You see, all loans have closing costs, and all lender have to charge for and cover the same closing costs. They all have to collect and pass on the same third party fees, such as appraisal, credit report, title company fees, state taxes, escrows, etc. Next, all lenders have to pay Loan Officer, processors, underwriters, and more, so they all have essentially the same lender related costs, like loan origination fees, and processing fees.

How lenders disclose, label, and charge your closing costs can vary greatly, but you as the borrower will ALWAYS be paying them. Read my article on understanding how mortgage company,

Lower Closing Costs = Higher Rates. Higher rates = Lower Closing Costs

Simply put, the lowest rate & the lowest closing costs do not go hand-in-hand. NO LENDER can offer both together. I can give you rock bottom interest rates, but it will cost you in higher closing costs. I can give you very low, or even no closing costs, but that comes with higher interest rates. Good lenders typically quote their best rate in combination with covering all third party fees (appraisal, credit report, title company, state taxes, county recording fees, etc) with 1% origination.

The Best Question to Ask Yourself is:

"Which mortgage lender is going to charge me the least amount of money for the rate I want?"

Step-by-step process to get the "Best Deal" on Home Loans

- Pick the program that best suits your needs.

- Next, YOU choose the rate YOU want. By choosing the rate first you eliminate one giant shopping variable. You now can find out exactly which lender is charging you the least amount of money for the loan that you want.

- Closing Costs and Lender Fee's. PAY CLOSE ATTENTION. Many lenders will give you a ridiculous number that has no bearing on your real total costs by saying "OUR closing costs" or "OUR lender fee's" are X amount. Ask instead for the "bottom line", the "total amount required to complete the transaction", or even "what is the exact penny I will need to bring to closing?" By asking in this manner, you eliminate 99% of the misleading games some lenders play in attempting to make their costs sound so much better than everyone else. Please review the actual closing cost information listed below. Read Beware of the Bad Good Faith Estimate for more details.

- Ask the lender for a "Loan Estimate"(formerly known as a Good Faith Estimate - or GFE)" of settlement charges to verify if they are willing to put their pricing claim in writing. It is common, and OK if they give you something like a 'Fees Worksheet' and not the official federally mandated LE (loan estimate) at this stage. If refuse anything in writing, RUN! Make sure to tell them you want ALL costs from ALL sources involved in the transaction listed on the estimate. You do not want anything listed TBD (to be determined).

- Review each Estimate very carefully, especially if the estimate does not look exactly like a real final settlement statement (known as a "Closing Disclosure (or CD) Formerly known as HUD-1 Settlement statement). Double check to make sure that EVERY cost associated with your loan is listed. All REAL competitive estimates should be very close in total dollar amount!

On all The Joe Metzler Team Estimates, we always work diligently to make sure we ALWAYS include every single dollar required to complete the transaction, and for it to be as accurate as possible to what you will see on the day of closing. Because of this no surprise mentality, sometimes other estimates will unrealistically appear lower...

Still Confused? Fax or call me a copy of the other lenders Loan Estimate. I will be happy to review it with you. If it is a good estimate, I'll be the first to tell you. If it is a bad estimate, I'll help you understand how and why it is a bad estimate.

Will my estimated closing costs differ from the actual closing costs?

Yes, 100% it will be different In standard transactions, the difference between estimated and actual closing costs will vary slightly. The rules require that lenders Good Faith Estimate be very close, with just a small tolerance for variation. Therefore any variances should not normally be a cause for concern. These small differences between estimated and actual costs are a common source of confusion and frustration for borrowers. The main reasons for the difference between the estimated and actual costs are as follows:

Different investors charge different fees for processing your loan application. Therefore, if you are using a broker, they may not know the final real lender yet, and the actual investor’s origination cost, administrative fees, etc., may vary.

Your prepayment amount may vary. On a purchase, you might have to prepay certain expenses. To protect the collateral on their loan against your house, most lenders require you to prepay a year’s worth of insurance, as well as some property taxes up front. These amounts will vary and depend on many things, including the type of insurance you choose. You will also have to pay "days of interest" depending on what day of the month you close. This amount can vary greatly. We usually have no idea what day of the month you will be closing, so these costs are only estimated.

When you close. Pre-paid tax escrows vary greatly depending on the month you close. If we originally estimated your closing for January 25th, but you really close March 5th, the differences could easily be several hundred dollars.

Other fees may vary depending on which investor provides services for your application. For example, different title companies and appraisers have slightly different fee schedules, although they should be very close.

Can my final closing costs change dramatically from my initial estimate?

In theory, no. In reality, Yes. As I just mentioned, the rules require the lenders estimate to be accurate within a small tolerance. But, there is something known as a Change of Circumstance rules which allow a lender to significantly change the original Good Faith Estimate.

Legitimate change of circumstance examples:

- You locked the interest rate

- The loan amount changed (maybe you decided to put a bigger down payment)

- The program changed (maybe you went from an FHA loan to a conventional loan)

- The appraisal came in lower, so you needed to change the loan amount.

There is only a small number of legitimate Change in Circumstance changes officially allowed, but we hear of some lenders abusing this rule. For example, a lender is NOT allowed to change your estimate simple because they incorrectly quoted a fee they should have quoted correctly. Fees can not change that are not a result of a legitimate Change In Circumstance.

How do I pay closing costs?

There are essentially 4-ways to pay mortgage loan closing costs.

- Cash at closing out-of-pocket,

- Rolled into the purchase price (commonly known as Seller Paid Closing Costs)

- Rolled into a slightly higher interest rate (known as lender credits)A combination of any or all of these items

I don't like the term Seller Paid Closing Costs, because it implies the seller is paying your closing costs, so therefore they are free to the buyer. This is not true. Rather, seller paid closing costs is simply a way to pay your closing costs over time by rolling it into the purchase price, rather than have that out-of-pocket expense today.

An example would be you offered $100,000 for the home, and asked the seller to pay $5,000 of your closing costs. If the seller agrees, the seller is actually netting $95,000 in their pocket ($100,000 minus $5000). This means you really could have bought the house for $95,000 if you paid your own closing costs. This means then you are financing the $5,000 over the length of the loan instead of paying it out of pocket today.

The same goes with increasing your interest rate to lower or eliminate your out-of-pocket closing costs today.

Early on in the process you may also be required to pay for a credit report and the appraisal. Those fees will be listed on your estimate, but you will also see where those prepaid items get credit back on your final documents.

Finally at closing, you will need to bring a cashiers check or do a bank wire transfer of your down payment and any closing costs. Your Loan officer will give you the exact amount needed a few days before the actual loan closing.

** EXPERIENCE MATTERS **

Top rated mortgage lender locally and nationally, year after year... This is because clients agree - Experienced Loan Officers with mortgage interest rates you can brag about and amazing service clearly sets us apart from the big banks and online lenders.

Address

1549 Livingston Ave, Suite 105

Saint Paul, MN 55118Contact

Main (651) 552-3681

Joe@JoeMetzler.com

Cell/Text (651) 705-6261We also call from

(952) 486-6135License Info

Cambria Mortgage

NMLS# 322798 Branch:1888858Joe Metzler Sr Loan Officer/Branch Manager

NMLS# 274132. License MN #MLO-274132, WI #11418. SD #MLO.03095, ND #NDMLO274132, IA #36175, FL #LO119389, CO #100536785, AZ #LO-2016702Privacy Policies | Disclaimers | Disclosures | Terms of Use | DMCA Notice | ADA Notice |

Visit Our Social Media Pages

Equal Housing Lender. The Joe Metzler Team at Cambria Mortgage lends in Arizona, Colorado, Florida, Iowa, Minnesota, North Dakota, South Dakota , and Wisconsin only. This is not an offer to lend or to extend credit, nor is this a guaranty of loan approval or commitment to lend. Information here can become out of date, and may no longer be accurate. Products and interest rates are subject to change at any time due to changing market conditions. Not all programs available in all states. Actual rates available to you may vary based upon a number of factors. Consumers must independently verify the accuracy and currency of available mortgage programs. All loan approvals are subject to the borrower(s) satisfying all underwriting guidelines and loan approval conditions and providing an acceptable property, appraisal and title report. Joe Metzler, NMLS 274132, Cambria Mortgage NMLS 322798. © 1998 - 2026.