-

Share via:

(651) 552-3681

Home Purchase - Home Refinance

Lending in AZ, CO, FL, IA, MN, ND, SD, Wi

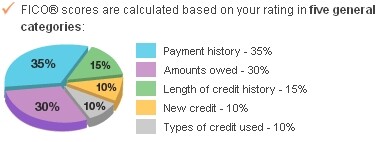

What credit score do I need for a home loan?

Generally speaking, in today's mortgage world, if your middle credit score is below 640, you are going to have a very difficult time obtaining a home loan. I didn't say impossible, I said very difficult. The further below 640, the harder it will be. For example, a 620 might still make it for a conventional loan, but under 620, that option goes away.

If you are below a 580 credit score, it is almost impossible to qualify for home loan financing no matter what anyone tells you, or what you read on the internet. Again, I didn't say no, I said almost impossible. You would need at least 10% down payment, and maybe higher. If you don't have that, don't even bother trying. While many lenders and loan programs appear to take lower credit scores, understand that credit score alone does not get you approved. With scores that low, you usually have plenty of other things on your credit report that will get you denied regardless of score, like recent late payments, foreclosures, etc.

FACT: Credit score alone does NOT equal a loan approval

With a score below 580, you really should save yourself the hassle. Stop attempting to find mortgage loans, and work on improving your scores instead. Once you have achieved a 620 or higher score, you should be in much better shape. If you are denied by a one lender, contacting 10 more probably won't help.

Visit Our Social Media Pages

Equal Housing Lender. The Joe Metzler Team at Cambria Mortgage lends in Arizona, Colorado, Florida, Iowa, Minnesota, North Dakota, South Dakota , and Wisconsin only. This is not an offer to lend or to extend credit, nor is this a guaranty of loan approval or commitment to lend. Information here can become out of date, and may no longer be accurate. Products and interest rates are subject to change at any time due to changing market conditions. Not all programs available in all states. Actual rates available to you may vary based upon a number of factors. Consumers must independently verify the accuracy and currency of available mortgage programs. All loan approvals are subject to the borrower(s) satisfying all underwriting guidelines and loan approval conditions and providing an acceptable property, appraisal and title report. Joe Metzler, NMLS 274132, Cambria Mortgage NMLS 322798. © 1998 - 2026.